Nickel, in its 99.99% purity grade — designated NP1 under the GOST 492 specification used across Russian, Indian, and Chinese precision-metals markets — is not the nickel of daily financial commentary. The nickel you read about in commodity-desk reports is overwhelmingly Class-2 nickel pig iron or ferronickel, produced at 10–30% purity for stainless steel alloying. Class-2 is a bulk commodity. It has an abundant ore base, its supply chain is concentrated in Indonesia and the Philippines, and its price signals are dominated by stainless-steel demand.

NP1 nickel is a different material, produced in a different manner, priced on a different curve, and consumed by an entirely different set of downstream industries. The distinction is not cosmetic. At the ppm-level trace-impurity specifications that NP1 meets and Class-2 does not, the material's behaviour in electrolyser cells, in turbine hot sections, and in EMI-shielded microelectronic housings is qualitatively different. Class-2 nickel cannot perform the work that NP1 performs. The reverse substitution — using NP1 where Class-2 would suffice — is economically irrational because NP1 trades at a structural premium.

This essay is about the applications that require NP1, the supply constraint on its production, and the industrial-demand reasons the market has not yet caught up to what this material does.

Application one: alkaline hydrogen electrolysers

The EU's REPowerEU hydrogen-economy build-out and the U.S. Inflation Reduction Act's hydrogen production tax credit have, together, set in motion a capacity-addition programme for alkaline water electrolysers that is unprecedented in its scale. An alkaline electrolyser's cell-stack uses nickel wire — drawn to diameters typically in the 0.05–0.20 mm range — as its catalytic electrode surface. The wire must be high-purity; at Class-2 impurity levels, the electrolyser's efficiency and lifetime collapse.

An industrial-scale alkaline electrolyser consumes meaningful quantities of precision-drawn NP1-grade wire per megawatt of installed capacity. At the EU's announced 100 GW alkaline-electrolyser capacity target for 2030, the implied feedstock demand on NP1 wire exceeds current announced precision-wire production capacity by approximately an order of magnitude. This is the single largest structural-demand signal in the precision-nickel market today, and it is only now beginning to be reflected in contract pricing.

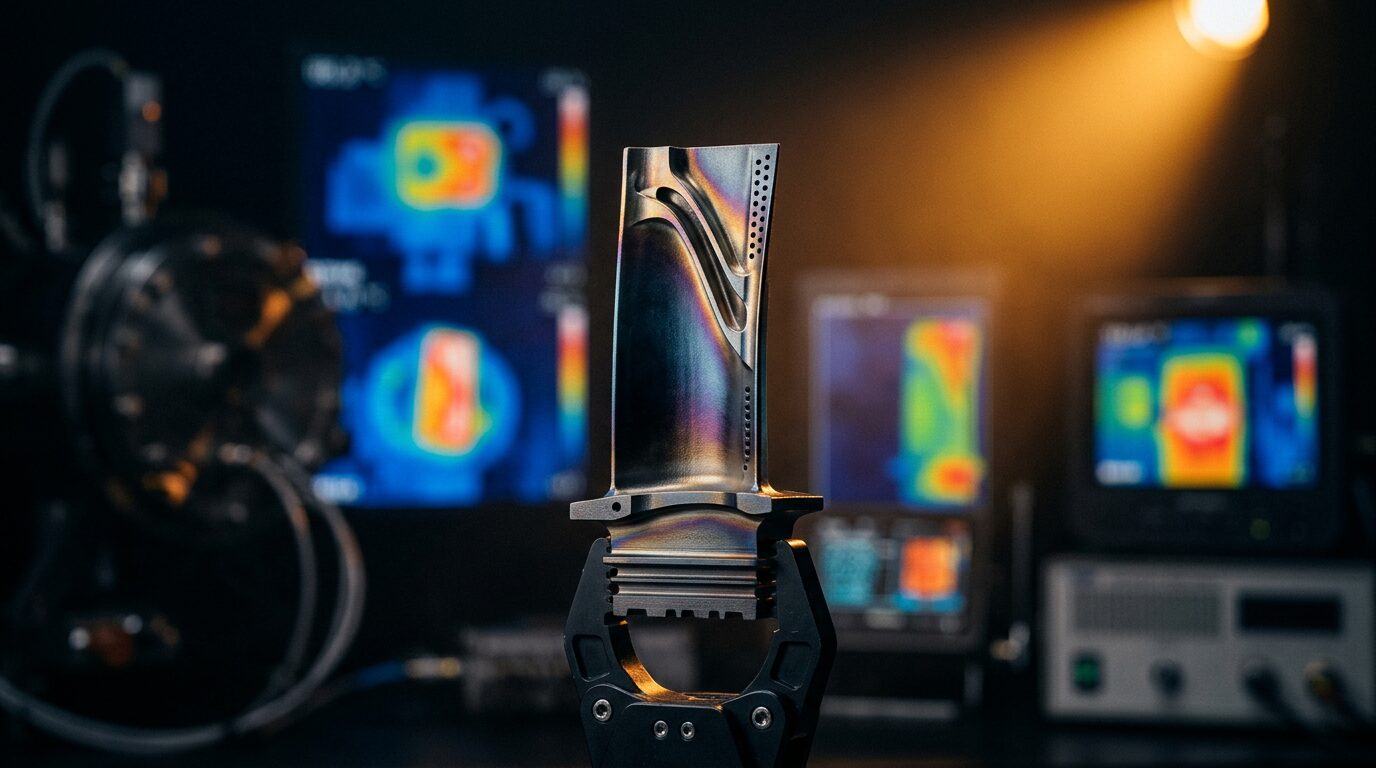

Application two: aerospace structural alloys

Nickel-based superalloys — Inconel 718, Inconel 625, René 41, and the newer single-crystal turbine-blade alloys used in high-pressure-turbine hot sections — are derived, in their precursor feedstocks, from ultra-pure nickel. The high-temperature creep performance of these alloys at 950–1,100 °C is bounded, at the ppm level, by trace-impurity chemistry in the feedstock. Class-2 nickel cannot serve this market at all.

The aerospace supply chain's demand for precision nickel is structurally rising on three independent vectors: commercial wide-body and narrow-body engine production rates, military fast-jet recapitalisation programmes (F-35, Tempest, AUKUS submarine reactor programmes), and the emerging supersonic and hypersonic airframe-development cycle. Each vector is lengthening its procurement horizon and tightening its feedstock specifications.

Application three: compound semiconductors

At the ppm-level trace-impurity specifications that NP1 meets and Class-2 does not, the material's behaviour in electrolyser cells, turbine hot sections, and EMI-shielded microelectronic housings is qualitatively different.

In gallium-nitride and silicon-carbide power-electronics fabrication — the fast-growing materials platforms that underlie electric-vehicle inverters, grid-tied power converters, and high-frequency radio-frequency infrastructure — ultra-pure nickel plays multiple roles: as an ohmic-contact metal on the chip itself, as a plated layer in the packaging, and as a shielding element in the module housing. The trace-impurity specifications required here are among the tightest in any industrial use. The global supply of nickel meeting this specification is, in a literal sense, counted in the thousands of tonnes per year.

Application four: EMI shielding

Electromagnetic-interference shielding in radio-frequency-sensitive electronics — medical imaging equipment, avionics, defence-grade sensors, 5G base-station electronics — requires a material with both high magnetic permeability and high electrical conductivity. Nickel occupies the narrow intersection of these properties at a price point competitive with the platinum-group metals. Precision-grade nickel foils and plated layers are the dominant EMI-shielding solution across this application space.

Application five: cryogenic structural components

Ultra-pure nickel retains ductility at cryogenic temperatures, making it the material of choice for LNG-tank internals, liquid-hydrogen-storage components, and spacecraft cryogenic-fluid systems. The ductile-brittle transition that limits most structural metals below –100 °C is, in ultra-pure nickel, essentially absent down to liquid-nitrogen temperatures.

Why the market has not caught up

Three structural reasons. First, the trade-reporting infrastructure for precision nickel is fragmented across small specialist producers and is not centralised in a single futures-market index; there is no "NP1 price" on Bloomberg's commodity screens in the way there is an LME Class-2 price. Second, the downstream demand reporting is fragmented across the sector literatures — electrolyser-industry analysts do not speak to superalloy analysts, who do not speak to semiconductor-materials analysts. Third, the structural thesis — that a single precision-metal specification is simultaneously the critical enabler of four or five independent industrial-demand vectors — has not been assembled in the published literature until recently.

This is the reason a regulated digital security backed by 7,026,905 metres of NP1 nickel wire, valued at USD 1.64 billion by an independent Aranca reserves report, is an instrument worth attention. The material the vehicle holds is the material the 21st century is quietly consuming. The market will catch up. It usually does. But while it catches up, the institutional positioning is available.

A note on supply

Precision-nickel refining capacity is concentrated in a small number of specialist producers in Russia (Norilsk's precision division), China (Jinchuan Group's precision output), and a handful of Western European specialist producers. Capacity additions in this subsector are on a multi-year lead time, require specialist infrastructure, and are limited by the availability of suitable ore-body feedstock with low trace-impurity baseline. The combination of rising end-application demand and slow-to-respond supply capacity defines, in classical commodity-market terms, the conditions under which precision-metal pricing enters a multi-year structural uptrend.

We are, in my assessment, at the beginning of such a period. The market has not yet named it. That is the window this publication exists to document.

Sources

- GOST 492-1973. Russian State Standard for Primary Nickel. Gosstandart / Rosstandart. 1 Jan 1973. https://docs.cntd.ru/document/1200000957 Accessed 10 Apr 2026

- Ramamurty, U. et al.. Trace Impurity Effects in Precision Nickel — a materials survey. Acta Materialia (forthcoming). 1 May 2026. https://www.sciencedirect.com/journal/acta-materialia Accessed 10 Apr 2026

- Aranca. ALKN Reserves Valuation. Aranca. 15 Mar 2026. https://alkemya.com/docs/aranca-2026-03.pdf Accessed 10 Apr 2026

- European Commission. REPowerEU — Hydrogen Plan. European Commission. 1 Mar 2023. https://commission.europa.eu/energy-climate-change-environment/repowereu_en Accessed 10 Apr 2026

- IIT Delhi Materials Department. NP1 Feedstock Validation — ALKN Reserves. IIT Delhi. 10 Nov 2025. https://www.iitd.ac.in/ Accessed 10 Apr 2026